Australia’s folding box market has declined over the last decade, writes IndustryEdge MD Tim Woods.

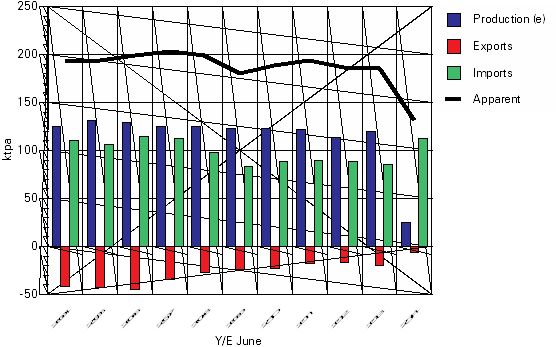

For most of the last decade, Australia’s folding box – or cartonboard – market was supplied with approximately 190kt of substrate, sourced from both the domestic producer and imports, and supplemented by an ever-growing volume of imported, pre-converted folding boxes. Following the closure of the Petrie Mill by Amcor in 2013, domestic production ceased altogether.

Significant inventories, in the hands of Amcor – and then Orora, as well as converters and brand owners, washed through the market at the same time as new imports commenced. At least some of the new imports were misclassified as coated woodfree printing and communication papers. The result of this was that apparent consumption declined dramatically on a single-year basis. The experience of the last decade is displayed in the chart below.

Australian Apparent Consumption of Coated Cartonboard: 2004 – 2014 (ktpa)

Source: ABS & IndustryEdge research and estimates

Industry participants consider any remaining inventories are fully worked through the market and that Australia is now fully supplied by imported coated cartonboard. Supplies of non-aseptic liquid packaging board, including cup stock, have been removed from this data.

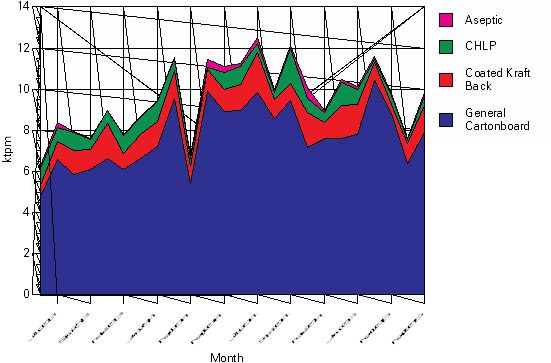

Full financial year data will be available later this month. For the year to the end of May 2015, imports have totalled 125.5 kt as the chart following shows. While that volume is the highest on record, the total import volume remains well below expectations, due to the import mis-classification. Industry participants are working with IndustryEdge to resolve the misclassification.

There are instances where IndustryEdge would take an accusatory tone where misclassification occurs. The industry is rightly wary of those who claim an ‘error’ to ‘hide’ a trade or worse, try to avoid a duty. But concur with those who find the tariff codes for coated cartonboard and coated woodfree printing and communication papers complex. They border on the bewildering and few have a complete handle on it.

Imports of Coated Cartonboard by Grade: Jun ’13 – May ‘15 (ktpm)

Source: ABS & IndustryEdge research and estimates.

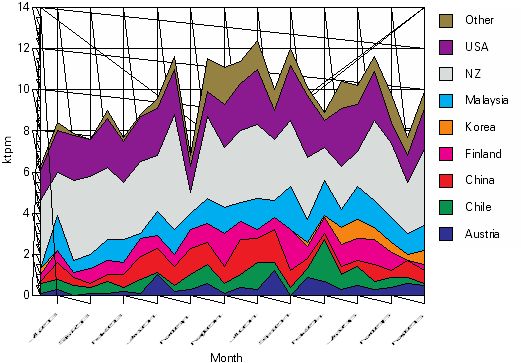

Because supply of substrate is fully imported, it is relevant to consider the country of origin of these same imports. The chart below shows that New Zealand continues to be the major supplier nation, but supply from the US is having an increasing influence. New Zealand’s supply is waning, as the sole producer – the Whakatane Mill, part of SIG Combibloc – completes its transition to the production of liquid packaging boards.

Imports of Coated Cartonboard by Country of Origin: Jun ’13 – May ‘15 (ktpm)

Source: ABS & IndustryEdge research and estimates.

Coupled with the closure of Petrie, the ‘swing’ of Whakatane has created a more dynamic import supply, which has in turn brought about the confusion of import data. However, supplies of substrate are not the only structural changes evident in the market.

Australian market structure

The structure of Australia’s folding box-board market is similar to most major packaging markets, in that a relatively small number of producers dominate delivery to a wide range of end-users. Inevitably, this gives rise to a very wide supply offering, which is considered to represent operational challenges in a small market.

Similarities between packaging sectors end at that point however, as this sector includes, among those holding significant market share, heavily integrated or diversified businesses (Orora, Hannapak), specialist cartonboard businesses that operate primarily at a single point in the supply chain but supply the widest possible group of end users (Colorpak) and businesses that dominate supply to one or more discrete end-use sectors (Anzpac Services).

Unlike the corrugated packaging market, which is dominated by Orora and Visy, there is evident fragmentation of the conversion sector, with almost 20 per cent of the sector supplied by smaller businesses.

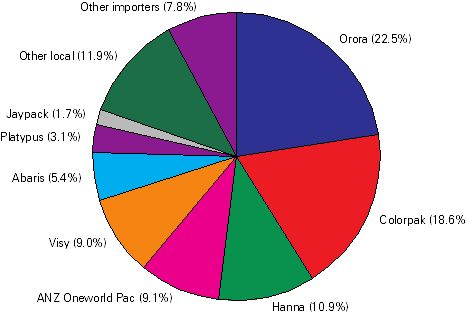

An alternative and more fully inclusive analysis of market shares was provided by Colorpak’s managing director Alex Commins in 2014 at IndustryEdge and Appita’s Packaging Market Outlook Forum. That market share analysis is reproduced below and segments what Colorpak estimates is an AUD645M market.

Folding Carton Market Shares: 2014 (%)

Source: Colorpak.

The purpose of showing this different analysis is not to create confusion. The Colorpak breakdown is of the entire market, inclusive of all products and categories. Based on other information related to liquid packaging boards, we consider the total market size to be closer to AU$700M or something close to 6.5 per cent higher than the Colorpak assessment.

What this breakdown reveals, provided by the major player with the greatest proportion of their skin in this particular game, is that the two largest companies hold just 44.1 per cent of the market. Compare this with the sibling corrugated box market, in which Orora and Visy together hold something close to 85 per cent of the market.

Hannapak, the division of the Hanna Group, has throughput of approximately 30kt per annum, but not all of that is cartonboard. Its production estimate is that it is ‘approaching one billion’ boxes per annum, across a staggering 2500 SKUs per year. Their apparent ability to deliver small runs, as well as large volume runs, is indicative of a market fragmenting in a variety of ways.

The growing market share of smaller converters and fully converted importers is telling for the sector. When the Petrie mill closed in 2013, domestic supply of substrate ended, but so too did the market’s ability to easily supply a very wide range of options, on short notice. If it was renowned for anything, Petrie’s capability in delivering whatever folding box configuration was required was a key advantage.

Over the two years since the end of domestic manufacturing, the market has evidently fragmented further, with growing market share for smaller converters and ever-increasing volumes of pre-converted imports filling supply gaps. Pre-converted imports are discussed in greater detail in the item leading into this analysis.

Based on import volumes, IndustryEdge considers the market’s structure has changed, with pre-converted cartonboard imports now accounting for as much as 27.5 per cent of the total market. Moreover, imports have grown over the last year, and average prices have increased sharply, as a result of the Australian Dollar’s depreciation.

The implication of rising pre-converted import prices is twofold. First, the domestic market struggles to meet the supply requirements that the imports deliver, making the imports reasonably resilient to price increases. Second, domestic prices have increased over the last year and the sector’s value has grown.

The volume of supply situation is displayed in the following pie chart, for the year to end of May 2015, which sets out imports by grade and includes the rising pre-converted imports as though a separate grade. The chart excludes imports of what are described as uncoated cartonboard, but which are generally considered to be the substrate imported for liquid packaging board production.

Coated Cartonboard Imports (inc. Pre-Converted) by Grade: Y/E May ‘15 (kt)

Source: ABS & IndustryEdge research & estimates

The suspicion has long been that the folding box market in Australia (and to a lesser extent, New Zealand) has not been extracting full value for its products and services. In part, this is because the sector is over supplied, both with capacity and by too long a tail of small producers, chasing the same markets.

Though it was a Petrie strength, the ability to deliver a very wide variety of SKUs from a domestic producer on relatively short supply lines and timeframes, created what became a market expectation. That expectation appears to be serviced increasingly, at least at the edges of the market, by a variety of converters and importers.

According to some, consolidation of converters, and rationalistaion of the market and supply, is required for the sector to extract full value for the advantage of the entire supply chain. However, some of the smaller converters that fill market gaps, contest that view, as do end-users whose unique requirements and expectations continue to be serviced by the sector.

End-users changing faster than the suppliers

Analysis of the Australian cartonboard market by its end uses, on a proportional basis, is described in the pie chart below. IndustryEdge has developed this analysis from information from Colorpak and additional analysis of retail and other sales volumes.

Cartonboard Supplies by End-Use: 2015 (%)

Source: Colorpak & IndustryEdge research and estimates.

The pace of consolidation in a number of these end-use sectors has been significant over the last half decade. In the key markets of Food, Pharmaceuticals and Beverage, consolidation has been rapid and is continual. While that creates opportunities to win tenders, it also creates challenges from losing tenders.

The result can be that a converter with a large capital footprint goes from being close to full capacity to well below capacity in the blink of an eye.

This has driven, to some extent, the folding box conversion sector’s over-capacity, making consolidation all the more urgent and yet, ever more difficult to achieve. That risk for the sector is ultimately a supply risk for end-users, some of whom are aware of the problem. Some are reportedly considering longer term supply contracts to encourage innovation and capital investment.

Prospects of rationalisation

In part because it is fully exposed to substrate imports, Australia’s folding boxboard market is under more pressure than ever before. Converters and their merchant suppliers are obliged to tightly manage inventories, yet must retain a volume of supply to meet quite diverse demand. The impact on margins can be acute, particularly in a conversion market that is over-capacity, faces constant challenges from the seemingly more innovative flexible packaging sector and that ultimately, seems to be overdue for a further round of consolidation.

The suspicion is that the value of folding boxes is not being rewarded in the market, with the prices that a rationalised sector could command. The sector’s fragmentation has seen pre-converted imports rise, further eroding domestic market opportunities and value.

Without overplaying the situation, IndustryEdge considers sector rationalisation cannot be far off. Perhaps how that will happen, remains the better question. For its part, Colorpak has done some heavy lifting. It consolidated the former Carter Holt Harvey operations in Australia into its business over the four years to the middle of 2014.

Orora, the largest player in the market and the large player with the greatest integration, is the logical player to make a rationalisation move. Their options are quite broad because any single acquisition would still see their market share below 50 per cent.

Others, including the always-capable Visy, could expand their share of the market through acquisition and rationalisation.

There is at least one other option being considered in the market.

The recent acquisition of Jalco by Pact Group Holdings gives rise to some options for consolidation. Jalco’s product lines include personal care and cosmetics, food and beverage and promotional packaging components, each of which uses, to some extent, folding boxes. It is not clear whether Pact’s strategic interests extend to the cartonboard sector, but there is speculation in the investor community about such a development being possible.

Rationalisation remains challenging however, in part because the cost of entry to the conversion sector is relatively low. Import competition is also an element of concern to those who might be considering rationalisation. Ultimately, those issues cannot be addressed in the market until there is sectorial consolidation and tighter integration.

Re-forming the box

Most of the discreet sectors of the Australian packaging market are rationalised or at least, undergoing consolidation that will lead to rationalisation. Such a move is overdue in the folding box conversion market and value seems to be the victim right now.

No party in the supply chain – including the end-users – is immune from the pressures.

Regardless of the importance of end-users, it is the converters that need to make the moves to improve the structure of the sector. It may not yet be urgent, but it is increasingly important, as fragmentation is demonstrating.

That said, we are only observing the beginning of a sector wide awareness and activity on the consolidation front. If that is the case, the situation of challenging value extraction may need to get tougher before it can get better.

Tim Woods is the managing director of IndustryEdge, a provider of market intelligence in Australia and New Zealand. It offers trade data and analysis in paper, paper products, pulp and recovered paper sectors.